In 2026, the Cebu property market is not a straightforward “buy anywhere” market—it is a market of contrasts, where location and property type determine everything. That’s the new reality. The days of automatic double-digit appreciation are over. Today, success depends on understanding where supply is tightening, where demand is growing, and where infrastructure spending is creating future value.

Introduction: The New Cebu Reality

For years, Cebu real estate was considered a sure bet. Buy almost anywhere near the city, wait a few years, and watch your investment grow. That era has ended. In 2026, the market has matured into something more complex—and more demanding of investors who do their homework.

Cebu now boasts the largest condominium supply outside Metro Manila, with stock reaching 92,300 units as of end 2025 and substantial completions expected through 2029. Yet, more than 10,000 housing units in Cebu alone are awaiting License to Sell approval, preventing developers from bringing new projects to market and tightening supply in certain segments. This contradiction—oversupply in some areas, shortage in others—defines today’s market.

This guide synthesizes current data, expert forecasts, and on-the-ground intelligence to answer a single question: Where should you invest in Cebu real estate between now and 2030?

Chapter 1: Market Overview—Where Cebu Stands Today

The Two Faces of Supply

Cebu’s residential market is being pulled in opposite directions.

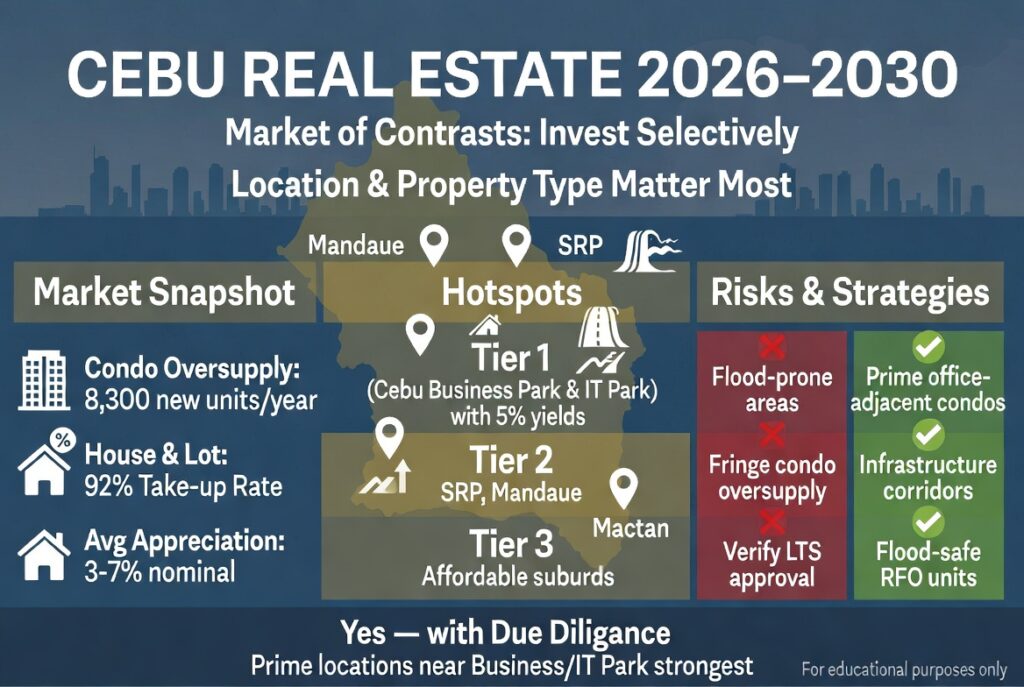

Condominium oversupply threatens rental yields in secondary areas. The condo pipeline remains aggressive. Colliers recorded 5,800 completions in 2024 and forecasts an average of 8,300 new condo units delivered annually from 2025 to 2028, pushing total stock past 102,500 units by 2027. That’s significant new supply competing for tenants and buyers.

House-and-lot and affordable housing remain undersupplied. The numbers tell a different story in this segment. Visayas and Mindanao house-and-lot developments posted a 92 percent take-up rate—meaning nearly every unit built found a buyer immediately. Lot-only developments followed closely at 86 percent. Affordable housing demand remains so concentrated that only about 10 percent of the market prefers larger units; the overwhelming majority want compact, affordable homes.

Price Trends: Real vs. Nominal Growth

What does this mean for prices? The answer depends on whose numbers you trust—and more importantly, which asset class you’re examining.

According to Bamboo Routes data, nominal appreciation registered at 3.8 percent year-over-year in the most recent reporting period. When adjusted for inflation, this translates to approximately 2.2 percent real growth. Rumavi’s analysis shows slightly stronger performance, with condominium values appreciating between 3 and 5 percent while gated houses posted 4 to 6 percent growth. Meanwhile, RichestPH reported more aggressive numbers, with quarterly comparisons showing 11.5 percent year-over-year growth and 12.2 percent quarter-over-quarter appreciation.

Looking ahead, two key supply-side data points matter for price forecasting. First, residential lot prices across Cebu rose by an average of 7 percent annually from 2016 to 2025. Some flagship projects achieved compound annual growth rates far above that average, with annual appreciation ranging from 8 percent to 27 percent in select developments. Second, new builds in Cebu typically cost 10 to 20 percent more than comparable existing homes, primarily because of better amenities and warranties. This suggests a persistent quality premium that should support prices for well-located new developments.

Rental Yield Reality Check

For income-focused investors, rental yields in Cebu remain respectable but vary dramatically by location.

Gross rental yields for prime condos in established business districts like Cebu IT Park deliver roughly 5 percent, particularly for studios and one-bedrooms that rent quickly to IT-BPM workers and students. According to Lamudi listing data, monthly rental prices in Cebu IT Park range from approximately ₱11,500 to ₱150,000, depending on unit size, furnishings, and amenities. At the higher end of the quality spectrum, well-located mid-range units often show faster turnover and strong monthly income, with high-end condos in Cebu generally yielding between 4.5 percent and 6 percent.

Chapter 2: Critical Market Shifts Reshaping Cebu Real Estate

The License-to-Sell Bottleneck

One of the biggest market distortions in 2026 is a regulatory bottleneck that most investors fail to consider. The Department of Human Settlements and Urban Development’s License-to-Sell approval process has slowed dramatically, with more than 10,000 housing units in Cebu alone awaiting clearance.

This bottleneck creates two opposing effects. First, there is artificial supply constriction in the affordable segment—units that could be sold are held back, keeping prices elevated. Second, there is major pre-selling risk for buyers—projects without LTS approval cannot be legally marketed, yet some developers begin taking reservations anyway. Investors in pre-selling condos must verify LTS status before committing any funds.

From 2016 to 2025, residential lot prices in Cebu appreciated an average of 7 percent annually. However, some notable projects posted compound annual growth rates as high as 27 percent, demonstrating that location and developer reputation create massive divergence in returns.

Economic Headwinds and Regional Risks

The broader economic environment adds another layer of complexity. The Philippine economy grew just 4.0 percent in Q3 2025, weighed down by sluggish household consumption and reduced government infrastructure spending. While Colliers expects a cautiously optimistic finish driven by holiday spending and remittances, the macroeconomic backdrop is less robust than in previous boom cycles.

For OFW investors—a critical driver of Cebu property demand—global geopolitical risks loom. Ongoing conflicts in the Middle East threaten remittance flows, with analysts warning that higher oil prices and regional instability could negatively impact the money sent home by overseas workers. That said, new remittance protection frameworks moving toward implementation in 2026 aim to cap fees and improve transparency, potentially boosting net purchasing power for overseas buyers.

Flood Risk Is Reshaping Buyer Behavior

Perhaps the most overlooked factor in Cebu real estate is flood vulnerability. Buyer caution has increased measurably in flood-prone areas, which face longer sales times and higher insurance costs.

Areas known to experience recurring flooding include Mabolo, with its low-lying terrain and drainage issues; Bonbon, Kalunasan, Guadalupe, Pardo, and Carreta, all located on or near floodways; and various coastal zones and riverbanks classified as danger zones by Cebu City.

Investing without verifying flood history is now a material risk. Developers are responding by offering greater transparency on flood risk and site vulnerabilities, with some projects now integrating flood-mitigation designs and drainage improvements.

Developer Competition Benefits Buyers

On the positive side, heightened competition among developers in 2026 is creating buyer-friendly conditions. More projects are offering energy-efficient designs and solar power integration, smart-home features and modern amenities, greater transparency on environmental risks including flood history, and competitive pricing as developers vie for discerning buyers.

Chapter 3: Demand Drivers—Who Is Buying and Why

The OFW Engine

Overseas Filipino Workers remain the most powerful driver of Philippine real estate demand. In the first quarter of 2026, approximately 17 percent of all household remittances were allocated to real estate investments, concentrated primarily in the affordable housing segment.

This sustained demand is not collapsing—it is rebalancing. The Philippine residential market in 2026 is undergoing a natural correction after years of aggressive growth, but OFW demand, family buying, and steady rental needs keep fundamentals alive across many market pockets.

For Cebu specifically, OFW interest focuses on affordable condos within the ₱3 to ₱7 million range, which captured nearly half of sales; house-and-lot developments with their 92 percent take-up rates; and properties in infrastructure-backed growth corridors.

Local End-Users and the Urban Shift

Within Cebu itself, a major demographic shift is underway. Land is becoming more expensive and scarce, especially in prime locations, pushing more residents toward vertical living. Condos offer a practical solution—affordable living in central areas with convenient access to work, schools, and entertainment.

The absorption rate confirms strong buyer appetite. A remarkable 89 percent of all condo units launched in Cebu between 2015 and 2025 have been sold, according to KMC Savills. That’s a remarkably healthy figure despite the surge in new supply.

Meanwhile, the suburbs are also seeing significant growth as buyers seek more space and lower prices outside the urban core. This creates a bifurcated market where both city-center condos and suburban houses can perform well—but for different buyer segments.

The Remote Work Factor

The post-pandemic shift toward hybrid and remote work continues to influence Cebu real estate. Tenants and buyers are prioritizing reliable internet infrastructure with fiber-ready buildings, proximity to lifestyle amenities rather than just workplaces, larger units that accommodate home offices, and suburban locations that offer more space at lower cost.

Condo rentals in IT Park or the South Road Properties typically run ₱15,000 to ₱30,000 per month, while beach apartments in Mactan or Moalboal can be found for ₱10,000 to ₱20,000—though the latter are more suited to lifestyle buyers than serious rental investors.

Chapter 4: The Office Market Signal

Why does office market data matter for residential investors? Because office vacancy rates are a leading indicator of residential rental demand. Where companies lease space, employees need housing nearby.

Vacancy Trends by Submarket

At the top of the performance ladder is Cebu Business Park, where office vacancy currently stands at just 9.3 percent. This low vacancy indicates strong rental demand for nearby condos. Cebu IT Park shows improving vacancy rates with healthy leasing activity. These two districts represent the strongest office markets in the province.

However, the picture changes dramatically in fringe areas, where office vacancy reaches 23.3 percent—a soft market that suggests caution for condo investments nearby. Mactan presents an even more challenging picture with 30.4 percent vacancy, indicating oversupply and warranting significant caution.

Cebu’s overall office vacancy rate fell to 11 percent in 2025 from 16.6 percent in 2024, driven by strong leasing activity in key areas such as IT Park and select fringe locations. However, CBRE now expects overall Cebu office vacancy to rise to between 18 percent and 22 percent by end-2026, higher than the earlier 15.4 percent forecast.

The reason for this reversal involves shadow supply and weaker-than-expected demand in secondary markets. This creates a clear signal for residential investors. Condos located near Cebu Business Park, with its 9.3 percent vacancy, and IT Park, with improving fundamentals, have strong rental prospects. Condos near fringe areas, with 23.3 percent vacancy, or Mactan, with 30.4 percent vacancy, face a much tougher rental market.

Chapter 5: Investment Hotspots 2026–2030

Tier 1: Prime Investment Districts

Cebu Business Park. With office vacancy at just 9.3 percent, this area has the tightest office market in Cebu—and that means strong rental demand for residential units. High-street rents in prime Metro Cebu locations now range from about ₱450 to as much as ₱2,000 per square meter per month, matching or even exceeding top-tier rates in parts of Metro Manila.

Cebu IT Park. As the province’s BPO hub, IT Park continues to attract young professionals and outsourcing workers. Rental yields of roughly 5 percent are achievable, especially for studios and one-bedroom units that cater to single tenants. The Wave Towers, a striking twin-tower development rising to 42 floors each in the heart of IT Park, exemplifies the caliber of projects drawing investor attention in this district.

Lahug. This prime residential area offers convenient access to both IT Park and Ayala Center. Its mix of mid-range and upscale developments appeals to a broad tenant base.

Tier 2: Infrastructure-Backed Growth Corridors

SRP (South Road Properties). This reclaimed area is poised for major growth as developers launch mixed-use projects and the government considers further infrastructure investment.

Mactan (select projects only). While Mactan’s office market shows 30.4 percent vacancy, not all Mactan real estate is created equal. Beachfront resort-condominiums and affordable pre-selling projects like Saekyung Ocean Residences, with Towers 3 and 4 now open for reservation, cater to different buyer segments—lifestyle investors and budget-conscious OFWs, respectively.

Mandaue City. With ₱3 billion in priority projects submitted for 2027, including road and drainage improvements and a modern city hospital, Mandaue is positioning itself for significant infrastructure-driven appreciation.

Tier 3: Underserved Affordable Housing Locations

The 92 percent take-up rate for house-and-lot developments in Visayas and Mindanao signals massive unmet demand for affordable housing outside prime districts. Locations within a 30 to 45-minute commute of Cebu City’s business districts, where land prices remain reasonable, represent the highest potential for price appreciation in the 2026–2030 period.

Chapter 6: Infrastructure Projects to Watch

Cebu’s long-term growth trajectory depends heavily on government infrastructure spending. Here are the key projects that will shape property values.

Water and Flood Control (Most Urgent)

Five dam projects have been endorsed as top priorities by the Provincial Development Council—these will address both water supply and flood mitigation. The Department of Public Works and Highways in Region 7 has endorsed 126 infrastructure projects for Cebu Province amounting to ₱23.2 billion for 2027. Seven proposed dams for Cebu in calendar year 2027 could see construction beginning as early as that year if funding is approved. The Metro Cebu flood control project, known as Oplan Kontra Baha, represents a major waterway improvement initiative.

Transportation

A proposed coastal road project aims to ease traffic congestion, with a feasibility study targeted for 2027. Various road and drainage improvements are planned across Mandaue City and other municipalities.

Commercial

SMX Cebu represents a ₱3.6 billion investment in a new MICE venue—meetings, incentives, conferences, and exhibitions—that will boost the province’s business tourism sector.

Investment Implication

Properties located near funded infrastructure projects typically see above-average appreciation in the three to five years following completion. The dam projects, in particular, will improve livability in surrounding residential areas by reducing flood risk and ensuring water security.

Chapter 7: Risks and Red Flags for Investors

Supply Overhang in Secondary Condo Markets

With 8,300 new condo units expected annually through 2028, secondary locations—those outside prime business districts—face genuine oversupply risk. Investors should avoid fringe-area condo developments unless they have a specific thesis about future infrastructure that will transform the location.

Pre-Selling Approval Risk

The LTS bottleneck has created a dangerous gray market. Some developers accept reservation fees for projects that have not yet received government approval. Buyers who commit to such projects face the risk of indefinite delays or, in worst-case scenarios, losing their deposits. Always verify that a project has a valid License to Sell before paying any money.

Flood Vulnerability

Flood risk is no longer a secondary consideration. Properties in flood-prone areas face slower sale times and longer vacancy periods, higher insurance premiums, and potential for significant damage during typhoon season. Before purchasing any property, request flood history data and consider consulting local drainage maps.

Office Oversupply in Certain Zones

The office vacancy forecasts for fringe areas at 23.3 percent and Mactan at 30.4 percent should give residential investors pause. Low office occupancy means fewer workers needing nearby housing—which translates to weaker rental demand and longer vacancy periods for condos in those locations.

Regional Economic Sensitivity

Cebu’s economy remains heavily exposed to BPO sector performance and OFW remittance flows. A global economic slowdown, Middle East conflict escalation, or major disruption to outsourcing operations would directly impact both rental demand and property values.

Chapter 8: Actionable Investment Strategies for 2026–2030

Strategy 1: Focus on Prime Office-Adjacent Locations

Target condos within 1 kilometer of Cebu Business Park or IT Park. This strategy works because office vacancy at 9.3 percent in the Business Park ensures steady tenant demand from BPO workers and professionals. Gross rental yields of 5 percent are achievable. The risk level is low to moderate.

Strategy 2: Buy Affordable Housing in Infrastructure Corridors

Target house-and-lot or affordable condo developments in municipalities along planned infrastructure routes. Take-up rates of 92 percent confirm massive unmet demand. As roads and flood control projects complete, these areas become more livable and accessible, driving price appreciation. The risk level is moderate, dependent on infrastructure timelines.

Strategy 3: Avoid Fringe-Area Pre-Selling Condos

Avoid condo developments more than 2 kilometers from either Business Park, IT Park, or a confirmed infrastructure node. With 8,300 annual completions through 2028, secondary markets will be flooded with supply, pressuring both rental yields and resale values.

Strategy 4: Prioritize Flood-Safe Properties

Check flood maps, elevation data, and developer disclosures about drainage systems. Flood risk is now priced into buyer behavior. Safe properties command premium values; vulnerable properties face discounting.

Strategy 5: For OFWs—Prefer RFO or Near-Completion Units

Target ready-for-occupancy units or projects scheduled for completion within 12 months. The LTS bottleneck makes pre-selling timelines unpredictable. RFO units eliminate completion risk and allow immediate rental income generation.

Conclusion: Is Now the Time to Invest?

Yes—but selectively, and with due diligence.

The Cebu real estate market of 2026 is not the easy-money market of 2016. Success requires location precision—condos near business districts remain strong; fringe-area condos face headwinds. Success requires asset class awareness—house-and-lot and affordable housing outperform luxury segments. Success requires risk avoidance—verify LTS status, check flood maps, and avoid oversupplied submarkets. Success requires infrastructure awareness—properties near funded projects will see above-average appreciation.

For investors who do their homework, Cebu still offers compelling opportunities. The province’s geographic constraints—limited land in Metro Cebu—create natural supply limitations that will continue supporting prices in prime locations. The construction industry in the Philippines is predicted to achieve an impressive annual growth rate of 7.2 percent from 2026 to 2029, signaling sustained development momentum.

The developers expanding outside Metro Manila are prioritizing Cebu as a key market for new malls, lifestyle centers, and retail spaces, reinforcing the province’s status as the country’s most important regional property market. Cebu remains the number one real estate destination outside the National Capital Region, and that ranking is unlikely to change through 2030.

But the era of blind investment is over. In 2026, the winning investor is the informed investor—the one who checks the LTS, verifies the flood map, analyzes the office vacancy rate, and invests where demand outpaces supply.

Sources for this report: Bamboo Routes, BusinessWorld Online, CBRE Philippines, Cebu Daily News, Colliers International, KMC Savills, Lamudi Philippines, Philstar, RichestPH, Rumavi, SunStar Cebu, and Ziggurat Real Estate.

This information is for educational purposes and should not be considered financial advice. Consult with licensed real estate professionals before making investment decisions.

🔍 Next Steps for Your Investment Journey

- Read Next: The Complete Guide to Buying Real Estate in Cebu (2026 Edition)

- For OFWs: OFW Guide to Buying Property in Cebu Without Scams

- Is Mactan still a good investment ?

Contact Us

Author

John Paul Ybañez Paquibot

Licensed Real Estate Broker | PRC No. 00014132 | DHSUD No. CVRFO-B-03/18-2672

Bachelors Realty and Brokerage, Inc. Cebu

G/F Cap Building, Brgy. Corner, Osmeña Blvd.

Arlington Pond St. Extension, Cebu City, 6000 Cebu