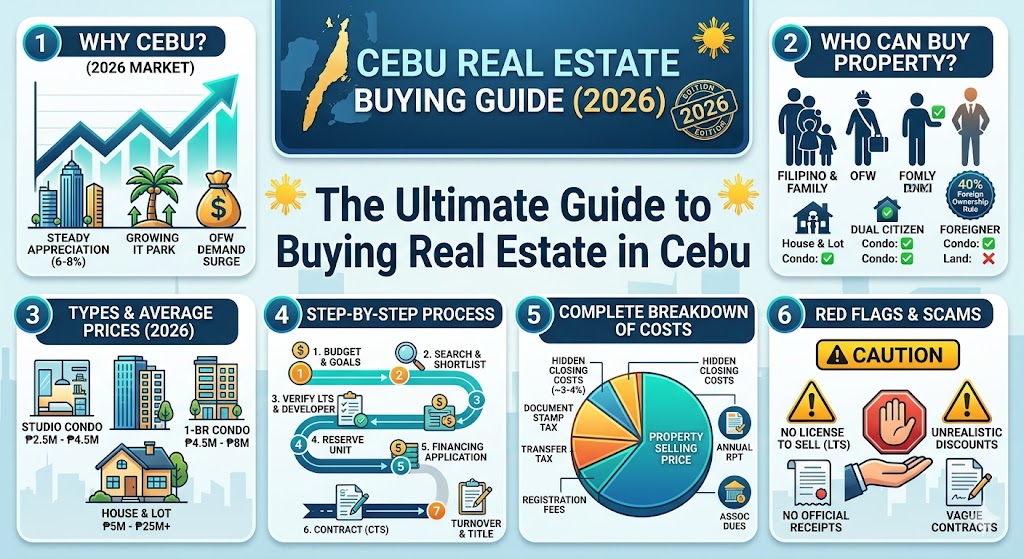

1. Why Cebu? The 2026 Market Snapshot

Cebu remains the second-largest real estate market in the Philippines after Metro Manila. In 2026, the market is showing three clear trends:

- Steady price appreciation – 6–8% annually in prime areas (Cebu IT Park, Cebu Business Park, Banilad, Lahug).

- Supply tightening – More than 10,000 housing units across Cebu are awaiting License to Sell (LTS) approval from DHSUD, creating artificial scarcity for ready-for-occupancy (RFO) units.

- OFW demand surge – 17% of household remittances in Q1 2026 went to real estate purchases, concentrated in the ₱2M–₱5M price range.

Key takeaway: 2026 is not a “buy anything and profit” market. Location and developer reputation matter more than ever.

2. Who Can Buy Property in Cebu?

Understanding who is legally permitted to purchase real estate in Cebu is essential before beginning your investment journey. The rules vary significantly based on citizenship status and the type of property involved.

Filipino citizens face no restrictions whatsoever. They can freely purchase condominiums, house-and-lot developments, townhouses, and raw land anywhere in Cebu without limitation.

Overseas Filipino Workers who hold Philippine passports enjoy the same rights as citizens residing in the country. Their status as OFWs does not impose any additional restrictions on property ownership.

Dual citizens who hold both Philippine and foreign citizenship can also purchase property freely, provided they can present their dual citizenship papers to verify their status.

Foreign nationals who are not Filipino citizens face significant restrictions under Philippine law. They are permitted to purchase condominium units, but only up to the maximum 40 percent foreign ownership limit per condo project. However, they are absolutely prohibited from owning land, which means house-and-lot properties are off-limits.

Foreigners married to Filipino citizens have a specific pathway to property ownership. While the foreign spouse cannot hold title to land, the couple can purchase a house-and-lot property provided the title is placed under the Filipino spouse’s name. This arrangement is legally sound as long as the marriage is valid and the property is considered conjugal.

Corporations can purchase property in Cebu, but strict rules apply. The company must comply with the 60/40 rule, meaning at least 60 percent of the corporation must be Filipino-owned. The corporation must also be properly registered with the Securities and Exchange Commission.

An important clarification for foreign investors: while foreigners cannot own land in the Philippines, they can legally own a condominium unit in Cebu. For those interested in landed property, long-term lease agreements are possible, extending up to 50 years with an option to renew for another 25 years.

3. Types of Real Estate You Can Buy in Cebu

Different property types serve different investment goals and buyer profiles. Understanding the options available and their typical price ranges is crucial for making informed decisions.

Studio condominiums ranging from 18 to 25 square meters represent the entry point for many investors. These units typically cost between ₱2.5 million and ₱4.5 million as of 2026. They are best suited for single professionals and Airbnb investors seeking affordable urban living spaces.

One-bedroom condominiums measuring 30 to 40 square meters offer more living space and appeal to couples and small families. Prices range from ₱4.5 million to ₱8 million, making them a popular mid-range option.

Two-bedroom condominiums spanning 45 to 70 square meters cater to families and long-term renters who need additional space. These units command prices between ₱7 million and ₱15 million.

House and lot properties within subdivisions continue to be the preferred choice for families and OFWs planning for retirement. Prices vary widely from ₱5 million to over ₱25 million depending on location, size, and developer reputation.

Townhouses offer a budget-friendly alternative to single-detached homes, typically ranging from ₱3.5 million to ₱8 million. They appeal to cost-conscious families who still desire landed property.

Raw lots are purchased by investors who plan to build their own homes or hold land for future appreciation. Prices per square meter range dramatically based on location, from ₱15,000 in developing areas to ₱80,000 or more in prime districts.

4. Step-by-Step Buying Process

Purchasing property in Cebu follows a structured process that typically spans several months to years, depending on whether you choose pre-selling or ready-for-occupancy units.

Step 1: Define Your Budget and Goals

The first phase requires two to four weeks of careful planning. Calculate the total cash you can spend, including equity payments, closing fees, and moving costs. Decide whether your purchase is for investment purposes, such as rental income or Airbnb operations, or for personal use. If you plan to finance the purchase, check your credit score to assess your eligibility for bank financing.

Step 2: Search and Shortlist

Allow four to eight weeks for this crucial phase. Use online portals like Lamudi, Property24, and Facebook Marketplace, and also visit developer showrooms directly. For pre-selling properties, inspect model units and review project plans. For ready-for-occupancy units, schedule actual site visits. A critical step many buyers skip is checking traffic patterns during rush hour—Cebu traffic is a significant factor that affects property desirability and resale value.

Step 3: Verify Developer and Project Legitimacy

Dedicate at least one week to due diligence. Verify that the project holds a valid License to Sell from the Department of Human Settlements and Urban Development. Check the developer’s Certificate of Registration. Research the developer’s track record, including completed projects, turnover delays, and any complaints lodged by previous buyers. This step cannot be overemphasized—skipping it has cost many investors dearly.

Step 4: Reserve the Unit

Once you’ve selected a property, you will pay a reservation fee typically ranging from ₱10,000 to ₱50,000. This fee is generally non-refundable, so be certain of your decision. Sign the Reservation Agreement and read the cancellation clauses carefully before committing.

Step 5: Apply for Financing

This phase typically takes two to four weeks. You have three main options. Bank loans offer up to 80 percent of the appraised value at interest rates of 7 to 9 percent per annum as of 2026. The Pag-IBIG housing loan provides lower rates but stricter requirements, requiring at least 24 monthly contributions. In-house financing is convenient but expensive, with interest rates ranging from 12 to 18 percent per annum.

Step 6: Execute the Contract to Sell

This step takes one to two weeks. Review every page of the contract carefully, paying particular attention to the payment schedule, delivery date, and penalties for delays. The contract must be notarized to be legally binding.

Step 7: Pay Equity or Down Payment

Depending on whether you purchased a pre-selling or RFO unit, this phase lasts six to twenty-four months. Pre-selling units typically allow monthly installments with zero interest over the construction period. Always obtain official receipts for every payment made.

Step 8: Loan Takeout and Turnover

Approximately 30 to 90 days after project completion, the bank releases loan proceeds to the developer. The developer issues a Notice of Turnover, and you must inspect the unit within seven days. Document any defects through a punch list before signing the acceptance documents.

Step 9: Move-in and Transfer Title

This final phase takes three to twelve months after full payment. The developer processes the Certificate of Completion and Tax Declaration. The buyer pays transfer taxes, registration fees, and documentary stamp tax. Finally, the Transfer Certificate of Title for house-and-lot properties or Condominium Certificate of Title for condo units is issued in your name.

5. Complete Breakdown of Costs and Hidden Fees

Many first-time buyers budget only for the selling price, unaware of the substantial additional costs involved. Here is the complete picture of what you will actually pay.

Upfront Costs Before Turnover

The reservation fee ranges from ₱10,000 to ₱50,000 and is paid by the buyer. This fee is non-refundable if you decide to back out of the purchase.

The equity or down payment typically represents 10 to 30 percent of the purchase price, payable in installments over the construction period for pre-selling units.

If you are financing your purchase, expect to pay a loan application fee of ₱5,000 to ₱15,000 and an appraisal fee of ₱3,000 to ₱8,000, both of which are the buyer’s responsibility.

Hidden Closing Costs at Turnover and Title Transfer

These costs catch many buyers by surprise, as they are not included in the selling price and must be paid in cash before you receive your title.

Documentary stamp tax amounts to 1.5 percent of the property price. For a ₱5 million condo, this equals ₱75,000.

Transfer tax ranges from 0.5 to 0.75 percent of the property price, or ₱37,500 for the same ₱5 million property.

Registration fees paid to the Land Registration Authority range from 0.25 to 0.5 percent of the property price, approximately ₱12,500.

Title issuance fees for a new Condominium Certificate of Title are approximately ₱15,000 fixed.

Notarial fees typically range from ₱5,000 to ₱15,000, with miscellaneous costs like mailing and documentation adding another ₱5,000.

Total closing costs generally amount to approximately 3 to 4 percent of the property price. For a ₱5 million condo, expect to pay roughly ₱155,000 in closing costs alone.

Three Surprises First-Time Buyers Miss

Surprise number one: Closing costs are not included in the selling price. You must pay them in cash before you get your title. Many buyers are shocked to discover they need an additional ₱150,000 to ₱200,000 at turnover.

Surprise number two: Real property tax is annual and recurring. For a ₱5 million condo, expect to pay between ₱15,000 and ₱25,000 per year. Developers sometimes prorate the first year’s tax, but you will be responsible for subsequent years.

Surprise number three: Association dues range from ₱80 to ₱150 per square meter per month. A 40-square-meter unit would therefore incur monthly dues of ₱3,200 to ₱6,000, even if the unit remains vacant. This is an ongoing expense that many investors forget to factor into their cash flow projections.

6. Financing Options Compared

Cash Purchases

Cash buyers enjoy the best position, paying zero interest and often negotiating discounts of 5 to 10 percent off the listed price. This option is ideal for those with substantial savings and eliminates the complexity of loan applications.

Bank Loans

Local banks offer interest rates of 7 to 9 percent per annum as of 2026, with maximum loan terms of 20 years. Down payment requirements typically stand at 20 percent. This option works best for OFWs with stable income and good credit standing.

Banks typically require valid government ID, proof of income through payslips and tax returns, and for OFWs specifically, employment contracts, visa documentation, remittance history, and a power of attorney if buying remotely. The bank will also conduct its own property appraisal before approving the loan.

Pag-IBIG Housing Loans

Pag-IBIG offers the most competitive rates at 6 to 7.5 percent per annum, with maximum loan terms of 30 years and down payments as low as 10 to 20 percent. This option is available to members who have made at least 24 monthly contributions.

In-House Financing

Developer-provided financing comes at significantly higher interest rates of 12 to 18 percent per annum, with shorter terms of 5 to 10 years and down payments of 10 to 30 percent. This option is best avoided unless you cannot qualify for bank or Pag-IBIG financing.

Critical advice: Never use in-house financing unless you have absolutely no other option. The high interest rates will consume your return on investment. If you must use it, treat it only as a bridge loan for 6 to 12 months while applying for bank loan takeout.

7. Red Flags and Scams to Avoid

Cebu real estate is generally reputable, but scams and problematic transactions do occur. Watch for these warning signs.

Developer Red Flags

A developer operating without a valid License to Sell is an absolute dealbreaker. Be highly suspicious of “soft launch” discounts that seem too good to be true, such as 50 percent off pre-selling prices. Developers who cannot provide a list of completed projects you can visit should be approached with extreme caution. Check social media platforms like the “Cebu Real Estate Buyers Watch” Facebook group for negative reviews and complaints. Be wary of promises guaranteeing rental income—only licensed property managers can legally make such claims.

Transaction Red Flags

If a seller requests payment via a personal bank account rather than an escrow account or the developer’s official corporate account, this should raise immediate concerns. The absence of an official receipt for your reservation fee is another warning sign. Review the Contract to Sell carefully for missing pages or altered dates. If the seller rushes you to sign without allowing time for a lawyer to review the documents, this is a significant red flag.

Online Scams on Facebook Marketplace

Exercise caution with postings that use blurry photos and fail to provide an actual address. Listings priced at 40 percent or more below the market average are almost certainly fraudulent. Sellers claiming to be “owner direct” but unable to provide a certified copy of the title should be avoided.

What to Do

Always request a certified true copy of the title from the Registry of Deeds and a tax declaration from the assessor’s office. Pay only after a lawyer or licensed real estate broker has validated all documents.

8. Legal Checklist: Documents to Verify Before Paying

Before giving any money, even a reservation fee, verify these five essential documents.

First, obtain the Condominium Certificate of Title for condo units or Transfer Certificate of Title for house-and-lot properties from the Registry of Deeds in Cebu City or Lapu-Lapu. Verify that the owner’s name matches the seller and that there are no liens, encumbrances, or annotations on the title.

Second, secure the Tax Declaration from the City Assessor’s Office. Confirm that real property tax has been paid up to the current year and that the assessed value is consistent with the property’s condition.

Third, request the License to Sell from DHSUD Region VII or directly from the developer. Verify that the license is valid and covers the specific unit and building phase you are purchasing.

Fourth, obtain copies of the Development Permit and Building Permit from the City Engineering Office to confirm that construction was legally approved.

Fifth, for condo projects, request the Certificate of Registration from the Securities and Exchange Commission to verify that the developer’s condominium corporation is properly registered.

Do not skip this step. Buyers have lost over ₱1 million because the seller did not actually own the property or the project had no valid License to Sell.

9. Pre-Selling vs. Ready-for-Occupancy

Pre-Selling or Off-Plan Purchases

Pre-selling properties offer lower prices with discounts of 10 to 20 percent compared to RFO units. Payment terms are more flexible, with equity stretched over 12 to 36 months at zero interest. However, move-in timelines extend to 2 to 5 years with the risk of construction delays. There is also the risk of developer insolvency, quality changes from the original plans, and project cancellation.

The return on investment potential is higher if the property appreciates during construction. Pre-selling is best suited for long-term investors with patience who can wait for the project to complete.

Ready-for-Occupancy or RFO Units

RFO properties command higher prices with a market premium but offer the certainty of seeing the actual unit before purchase. Payment involves a lump sum or standard loan. Move-in is possible within 30 to 60 days, with low risk of delays or quality issues.

Immediate rental income is possible from the day of turnover. RFO units are best for end-users and risk-averse buyers who want certainty.

2026 Specific Advice

For pre-selling purchases, choose established developers like Ayala Land, SMDC, Megaworld, Filinvest, or Rockwell. For boutique developers such as Plumera Residences, conduct extra due diligence by visiting their past projects and speaking with existing homeowners.

10. Neighborhood Guide: Where to Buy in Cebu

Prime Locations: High Appreciation, High Entry Price

Cebu IT Park commands prices of ₱150,000 to ₱220,000 per square meter for condominiums. Rental yields range from 6 to 8 percent, driven by the BPO workforce, expatriate tenants, and consistently high rental demand. This area is ideal for investors targeting BPO employees and young professionals.

Cebu Business Park sits at the luxury end with prices of ₱160,000 to ₱250,000 per square meter. Rental yields of 5 to 7 percent are achievable, making this area suitable for luxury buyers seeking long-term capital gains and premium tenants.

Banilad offers more moderate prices of ₱120,000 to ₱180,000 per square meter. Rental yields of 6 to 7 percent attract families drawn to the area’s excellent schools including Bright Academy and Cebu Doctors’ University. This neighborhood balances accessibility with family-friendly amenities.

Emerging Locations: Good Value, Growth Potential

Mandaue City, particularly near AS Fortuna, offers condominium prices of ₱90,000 to ₱130,000 per square meter. Rental yields of 6 to 9 percent reflect the affordable pricing and proximity to industrial zones. This area appeals to workers in nearby factories and commercial establishments.

Lapu-Lapu City in Mactan provides condominium prices of ₱80,000 to ₱120,000 per square meter. Exceptional rental yields of 7 to 10 percent are achievable through Airbnb and tourism-related rentals, driven by the proximity to the airport and beach resorts.

Talisay City offers the most affordable entry point at ₱60,000 to ₱90,000 per square meter. Rental yields of 5 to 7 percent attract budget-conscious buyers and those interested in land banking for future appreciation.

Overhyped Locations: Proceed with Caution in 2026

The South Road Properties, despite significant marketing attention, has many stalled projects and incomplete infrastructure. Buyers should exercise caution and investigate the status of specific developments thoroughly.

Consolacion and Liloan face severe traffic congestion during rush hour, and there is an oversupply of low-cost subdivisions that may pressure resale values. While prices appear attractive, the commute challenges can limit tenant demand.

11. Frequently Asked Questions (FAQ)

Q: Can I back out after paying the reservation fee?

A: Yes, but you lose the reservation fee (non-refundable). If you’ve already signed the Contract to Sell and paid equity, you may also lose a portion (read the cancellation clause).

Q: How long does it take to get the condo title under my name?

A: After full payment, expect 3–12 months. Delays are common due to backlog at the Registry of Deeds.

Q: Do I need a lawyer to buy a condo in Cebu?

A: Not legally required, but highly recommended – especially for pre-selling or secondary market (resale) purchases. Budget ₱20k – ₱50k for legal review.

Q: Can an OFW buy a condo without flying to Cebu?

A: Yes. You can execute a Special Power of Attorney (SPA) authorizing a trusted relative or your broker to sign documents on your behalf. The SPA must be notarized at the Philippine embassy in your country of work.

Q: What happens if the developer delays turnover for years?

A: Under Maceda Law (Republic Act 6552), if you have paid at least 2 years of installments, you can request a refund of 50% of total payments (plus 5% per additional year). For less than 2 years, you get a smaller refund. Many buyers never actually claim this – it’s a long legal process.

Q: Is Airbnb allowed in Cebu condos?

A: Depends on the condo’s Master Deed and Declaration of Restrictions. Some projects (e.g., in Mactan) allow short-term rentals; many in IT Park prohibit stays under 30 days. Always check before buying for Airbnb.

12. Final Checklist Before You Sign

Print this page. Tick every box before you pay anything. Download PDF file

- [ ] Budget – I have calculated total cash needed (equity + closing costs + association dues + taxes)

- [ ] Developer – I have verified LTS, track record, and online reviews

- [ ] Title – I have seen a certified true copy of the CCT/TCT (no encumbrances)

- [ ] Tax Declaration – Property taxes are fully paid

- [ ] Contract to Sell – I have read every page, especially delivery date and penalties for delay

- [ ] Financing – I have pre-approval from bank/Pag-IBIG (or cash ready)

- [ ] Legal review – My lawyer or licensed broker has reviewed all documents

- [ ] Payment receipts – I will get official receipts for every payment, never cash without receipt

- [ ] Move-in inspection – For RFO units, I will inspect within 7 days of turnover notice

Final Word From SEEKCEBU.com

Buying real estate in Cebu in 2026 can still build wealth – but only if you avoid the hidden costs, document traps, and overhyped locations. This guide gives you the complete roadmap. Use it.

Have questions about a specific condo project or developer?

Contact us through SEEKCEBU.com or join our Facebook community: “Cebu Real Estate Buyers (No Scams Allowed).”

Contact Us

Author

John Paul Ybañez Paquibot

Licensed Real Estate Broker | PRC No. 00014132 | DHSUD No. CVRFO-B-03/18-2672

Bachelors Realty and Brokerage, Inc. Cebu

G/F Cap Building, Brgy. Corner, Osmeña Blvd.

Arlington Pond St. Extension, Cebu City, 6000 Cebu