Buying a condo remains a major milestone for many Filipinos. For those eyeing units at Plumera Residences in Mactan, Cebu (developed by Johndorf Ventures), choosing the right home financing option directly impacts your monthly budget and long-term financial health.

In 2026, the two main choices are the Pag-IBIG Fund (government-backed) and traditional bank loans. They differ in interest rates, terms, down payment requirements, approval speed, and eligibility. This updated guide breaks down both options to help you decide what works best—whether you’re an OFW, first-time buyer, or young professional.

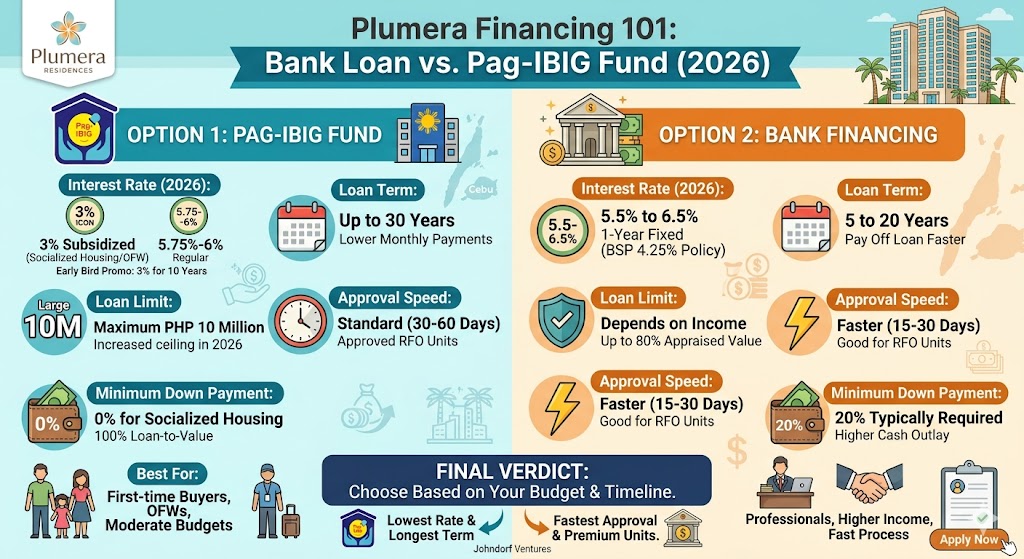

Option 1: Pag-IBIG Fund (Government-Backed Housing Loan)

Overview

Pag-IBIG Fund continues to be the most affordable and accessible option for many middle-income earners and first-time homebuyers. In 2025, it released a record ₱140.54 billion in housing loans to nearly 91,000 borrowers, demonstrating strong support for Filipino homeownership.

Key Interest Rates in 2026

- Subsidized 3% rate under the Expanded 4PH Program for qualified first-time homebuyers (gross monthly income below ₱34,686 outside NCR; ₱47,856 in NCR). All OFWs qualify regardless of income.

- Early Bird Promo: The first 30,000 qualified borrowers can enjoy the 3% rate for the first 10 years (standard is 5 years).

- Regular Pag-IBIG loans start at around 5.75% depending on the fixing period.

- Additional perks: Up to ₱100,000 for home improvements and 100% loan-to-value (no down payment) for qualifying socialized housing units.

Loan Terms and Limits

- Maximum term: Up to 30 years (keeps amortizations low).

- Maximum loan amount: Recently increased to ₱10 million (from ₱6 million) as of May 2026.

Eligibility

- At least 24 monthly contributions (lump sum allowed to catch up).

- Age: Not more than 65 at application and 70 at loan maturity.

- No existing unpaid Pag-IBIG housing loan.

- Income threshold for 3% rate as noted above.

Application Steps

- Verify membership and contributions via Virtual Pag-IBIG or a branch.

- Prepare documents and secure a Certificate of Eligibility.

- Submit the Housing Loan Application (HLA) form online or in-person with property and developer documents (e.g., License to Sell).

Required Documents (summary)

- Employed: Payslip, Certificate of Employment & Compensation, latest ITR.

- Self-employed: Financial statements, DTI/SEC docs, bank statements.

- OFW: POEA-certified contract, proof of remittances.

Option 2: Bank Financing (Private Home Loans)

Overview

Private bank loans suit buyers needing faster processing, higher loan amounts, or more flexibility. Major banks (BDO, BPI, Metrobank, etc.) typically finance up to 80% of the appraised value.

Interest Rates in 2026

With BSP policy rates around 4.5%, bank home loan rates are competitive: 1-year fixed rates generally range from 5.5% to 6.5%+, depending on credit score, income, and bank promos. Rates can be higher for longer fixed periods.

Loan Terms and Limits

- Typical term: 5–20 years (some banks offer up to 30).

- Loan amount: Based on income and property appraisal (no strict ₱10M cap like Pag-IBIG).

Eligibility

- Filipino citizen (or dual), 21–70 years old at maturity.

- Stable income (often ₱40,000–50,000+ monthly gross).

- Good credit history and at least 2 years continuous employment.

Application Steps

- Check pre-approval to know your borrowing capacity.

- Compare bank offers.

- Submit full application with property documents once you choose a unit.

Required Documents (summary)

Application form, proof of income, IDs, employment certificate, and Contract to Sell.

Head-to-Head Comparison: Pag-IBIG vs Bank Loan (2026)

Feature

Pag-IBIG Fund 3% subsidized (qualified), ~5.75% regular

Bank Financing 5.5%–6.5%+ (1-year fixed)

Max Loan Term

Pag-IBIG Fund Up to 30 years

Bank Financing 5–20 years (some up to 30)

Approval Speed

Pag-IBIG Fund 30–60 days

Bank Financing Faster (15–30 days)

Down Payment

Pag-IBIG Fund 0% for qualifying socialized units

Bank Financing Typically 20%

Max Loan

Pag-IBIG Fund ₱10 million

Bank Financing Higher potential based on income

Best For

Pag-IBIG Fund First-time buyers, OFWs, lower budgets

Bank Financing Strong credit, higher-value units, speed

Paperwork

Pag-IBIG Fund Moderate

Bank Financing Stricter credit & income checks

Sample Monthly Amortization Examples (Approximate, for ₱4M loan)

- Pag-IBIG at 3% for 30 years: ~₱16,800–17,500/month.

- Bank at 6% for 20 years: ~₱28,600/month.

(Use official Pag-IBIG calculator or bank tools for precise quotes based on your profile.)

Final Verdict: Which One Should You Choose?

Choose Pag-IBIG if you:

- Want the lowest possible rate and longest term for affordable payments.

- Are a first-time buyer, OFW, or have moderate income.

- Prefer zero or low down payment.

Choose a Bank Loan if you:

- Need faster approval (especially for Ready-for-Occupancy units).

- Have strong income/credit and want to buy a higher-priced unit.

- Prefer shorter terms to pay off the loan faster.

Many buyers combine both (e.g., Pag-IBIG for part of the amount) or use bank bridging if needed.

Conclusion

Start by checking your Pag-IBIG eligibility online or visiting a branch. For banks, get pre-approvals from 2–3 institutions. Contact the Johndorf Ventures sales team for current Plumera unit pricing, availability, and any developer financing promos that can complement these loans.

Secure your financing early to lock in rates and move forward with your Contract to Sell.

Disclaimer: This article is for general information only and not financial advice. Rates and programs change—consult Pag-IBIG, a bank loan officer, or licensed advisor for personalized guidance based on your situation.

Contact Us

Author

John Paul Ybañez Paquibot

Licensed Real Estate Broker | PRC No. 00014132 | DHSUD No. CVRFO-B-03/18-2672

Bachelors Realty and Brokerage, Inc. Cebu

G/F Cap Building, Brgy. Corner, Osmeña Blvd.

Arlington Pond St. Extension, Cebu City, 6000 Cebu

Leave a Reply