The brochures for high-rise developments in Metro Manila, Cebu, and Davao all promise the same enticing dream: resort-style amenities, prime locations, and a completely hassle-free lifestyle. They prominently highlight a neat monthly bank amortization figure, making property ownership feel easily attainable.

What those glossy pamphlets rarely emphasize is that the purchase price is only the beginning. Owning a condominium in the Philippines comes with a recurring and occasional tail of expenses that can quietly fracture a household budget if you are caught off guard.

This guide pulls back the curtain on the most significant hidden costs of condo ownership, providing you with real-world figures and practical, actionable strategies to help you budget like a professional.

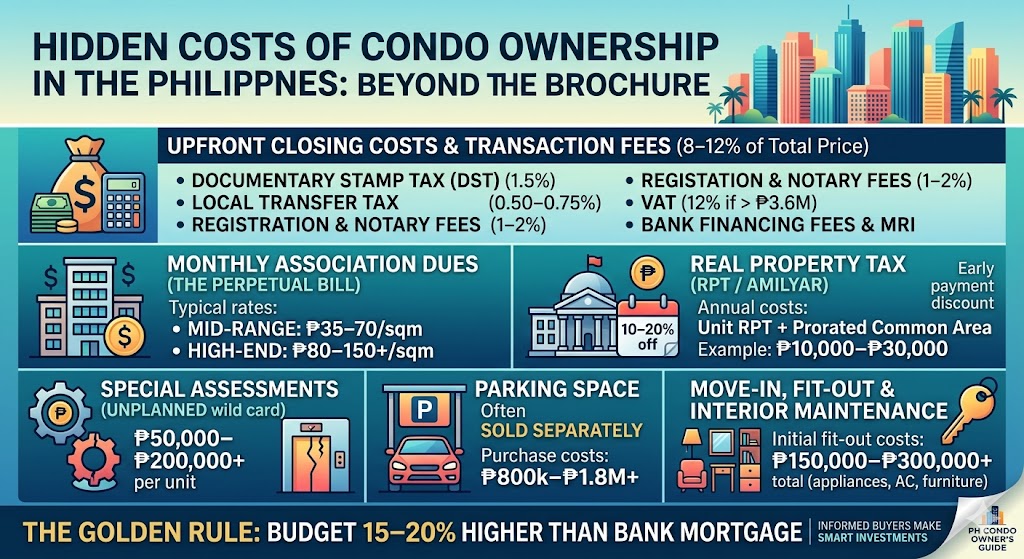

1. Upfront Closing Costs & Transaction Fees

When a developer says a unit is ₱5,000,000, your actual out-of-pocket cost to legally own it will be significantly higher. Closing fees are a massive, one-time surprise that typically add an extra 8% to 12% to the Total Contract Price (TCP).

- Documentary Stamp Tax (DST): Charged by the Bureau of Internal Revenue (BIR) at 1.5% of the selling price or zonal value, whichever is higher.

- Local Transfer Tax: Paid to the local government unit (LGU) to transfer ownership. It ranges from 0.50% in the provinces to 0.75% within Metro Manila cities.

- Registration & Notary Fees: Expect to spend around 1% to 2% to have the Deed of Absolute Sale legally stamped, notarized, and processed by the Registry of Deeds.

- Value-Added Tax (VAT): If you are buying a residential unit priced above the legal tax threshold (₱3,600,000), a heavy 12% VAT applies. Most developers quote new units as VAT-inclusive, but you must always confirm this in writing.

- Bank Financing Fees: If you are financing through a bank, you will pay a one-time Appraisal Fee (₱3,000 to ₱5,000) and processing fees, alongside mandatory bank-required insurances like Fire Insurance and Mortgage Redemption Insurance (MRI)—which protects the loan balance if something happens to you.

⚠️ The Capital Gains Tax (CGT) Trap: By law, the 6% CGT on a property sale is strictly the seller’s financial responsibility. However, in private resale transactions, sneaky sellers often try to insert hidden clauses into the contract forcing the buyer to cover it. Always review your contract terms line-by-line before signing, or you could face an unexpected bill of hundreds of thousands of pesos.

How to Prepare:

Demand a full, written breakdown of the “Other Charges” or closing costs from the developer or broker before paying any reservation fee. Do not assume these fees are automatically bundled into your equity or down payment schedule.

2. Monthly Association Dues (The Perpetual Bill)

You never truly finish paying for a condo. Even after your 20-year mortgage drops to absolute zero, you will owe monthly association dues for as long as you own the unit. These dues fund the building’s operations, covering security guards, pool chemicals, gym maintenance, elevator repairs, and common area electricity.

- Mid-range developments: ₱35 to ₱70 per square meter

- High-end / Prime locations (BGC, Makati, Rockwell): ₱80 to ₱150+ per square meter

The Math: If you own a modest 40-square-meter one-bedroom unit in a mid-tier building, you are looking at roughly ₱2,000 to ₱4,000+ per month. In luxury structures or prime business spots, annual dues can easily breach ₱80,000 to ₱120,000+ for larger spaces.

How to Prepare:

Before buying, request a look at the condo corporation’s latest financial statements and the size of its reserve fund (the emergency savings account for the building). A healthy reserve fund lowers the risk of sudden dues increases. Remember that if you fail to pay, the condo corp can legally strip your access to amenities, slap you with heavy interest penalties, and eventually declare your unit delinquent.

3. Real Property Tax (RPT / Amilyar)

In the Philippines, property owners must pay an annual Real Property Tax to the LGU. The rate is based on the property’s assessed value (which is determined by the local assessor’s office and is usually lower than the market value).

- The Rates: Up to 2% of the assessed value in Metro Manila cities, and 1% in most provinces.

- The Double Catch: You don’t just pay tax on your individual unit; you also pay a prorated share of the tax on the building’s common areas and the land it sits on. This common area tax is sometimes partially bundled into your monthly dues or billed as a separate, once-a-year invoice.

Realistic Example: For a standard condo unit with a market value around ₱3 Million to ₱5 Million, your annual RPT will often fall in the ₱10,000 to ₱30,000 range depending entirely on the city and its specific assessment level.

How to Prepare:

Check the exact tax rates with the local assessor’s office. Most LGUs offer generous early bird discounts (10% to 20% off) if you pay the full year’s amilyar in advance, usually before December 31st or January 31st. Always pay on time; late payments accrue a punishing penalty of 2% interest per month (capping at 72%).

4. Special Assessments (The True Wildcard)

Regular monthly dues are meant for daily operational costs, not structural emergencies. If a building’s roof leaks, the elevators break down completely, or the exterior facade needs a massive structural upgrade, the condo corporation levies a Special Assessment.

This is a mandatory, one-time bill distributed among all unit owners to cover major, unplanned capital improvements that the regular budget cannot absorb. These assessments can randomly demand anywhere from ₱50,000 to over ₱200,000 per unit, depending on the project’s scale. Older buildings or developments with poorly managed reserve funds carry the highest risk.

How to Prepare:

When buying a resale unit, request the last 2 to 3 years of Homeowners’ Association (HOA) meeting minutes. Current residents will actively voice concerns about upcoming repairs or structural defects in these meetings, giving you an insider look at potential looming assessments before you inherit them.

5. Parking (A Premium for Convenience)

A massive mistake first-time buyers make is assuming their condo automatically comes with a parking slot. It doesn’t.

Parking slots in the Philippines are sold under a completely separate property title and are rarely included in the unit’s base price.

- Separate Purchase: ₱800,000 to ₱1.8 Million+ per slot in highly urbanized business hubs.

- Monthly Rental: ₱3,000 to ₱7,000 per month if you lease from another owner.

How to Prepare:

Clarify the parking situation early in the process. If you do not drive but plan to lease the property out as an investment, research the local area carefully—condo units in heavy business districts without parking slots can suffer from significantly reduced rental appeal to premium tenants.

6. Move-In, Fit-Out & Ongoing Maintenance

Condo homeownership completely shifts the burden of interior upkeep onto your shoulders. The financial pressure doesn’t stop once the keys are turned over to you.

- Move-In / Turnover Fees: Developers frequently charge a one-time fee (ranging from ₱5,000 to ₱20,000+) to cover initial administrative setup, temporary elevator padding, and gate passes.

- Utility Deposits: You must settle connection deposits to your local electric provider (like Meralco), the water district, and internet service providers to get your meters activated.

- Initial Fit-Out Cost: Most units are delivered “bare” or “semi-furnished.” To make a studio or one-bedroom unit livable with basic appliances, an air conditioner, furniture, and closets, you need a liquid cash buffer of ₱150,000 to ₱300,000+ right at the start.

- Ongoing Maintenance: Unlike renting, if an air conditioner breaks down, a pipe leaks behind your kitchen drywall, or pest control is needed, you have to pay for the professional labor and materials out of your own pocket.

🧾 At-A-Glance Cost Summary

Closing Costs / Taxes

Frequency: One-Time (Upfront)

Typical Cost Range: 8% to 12% of property price

Key Buyer Advice: Get a written breakdown before paying a reservation; verify who pays the 6% CGT.

Association Dues

Frequency: Monthly (Recurring)

Typical Cost Range: ₱35 to ₱150+ per sqm

Key Buyer Advice: Review the building’s financial health report and the exact size of the reserve fund.

Real Property Tax (RPT)

Frequency: Annual (Recurring)

Typical Cost Range: 1% to 2% of assessed value

Key Buyer Advice: Pay early (usually by January) to claim local government discounts of up to 20%.

Special Assessments

Frequency: Unplanned (Occasional)

Typical Cost Range: ₱50,000 to ₱200,000+ per unit

Key Buyer Advice: Read historical HOA meeting minutes to check for upcoming structural repairs.

Parking Slot

Frequency: Upfront Buy / Monthly

Typical Cost Range: ₱800k–₱1.8M buy / ₱3k–₱7k rent

Key Buyer Advice: Clarify parking inclusion early; lack of parking can hurt future resale/rental appeal.

Move-In & Fit-Out

Frequency: Initial (One-Time)

Typical Cost Range: ₱150,000 to ₱320,000+ total

Key Buyer Advice: Budget conservatively for move-in fees, utility meter deposits, and basic furniture.

The Golden Rule for Condo Buyers

Condo living offers unparalleled benefits in terms of security, lifestyle, and proximity to major business districts. However, the shared nature of a high-rise building means you have less control over communal decisions and rising operational costs. To ensure your investment remains a financial sanctuary rather than a stressful trap, apply a rigid safety buffer to your math:

The 15–20% Buffer Rule: When budgeting for a condominium purchase in the Philippines, assume your actual monthly cost of living will be 15% to 20% higher than your projected bank mortgage payment alone.

If your monthly bank amortization is ₱25,000, your actual baseline cost to keep that lifestyle running smoothly—factoring in dues, taxes, and maintenance reserves—is closer to ₱29,000 to ₱30,000+.

Establish a dedicated home emergency fund from day one, do your thorough due diligence on the Master Deed, and run your numbers with cold transparency. By budgeting with your eyes wide open, you can fully protect your hard-earned capital and truly enjoy your new modern home without any financial surprises.

Contact Us

Author

John Paul Ybañez Paquibot

Licensed Real Estate Broker | PRC No. 00014132 | DHSUD No. CVRFO-B-03/18-2672

Bachelors Realty and Brokerage, Inc. Cebu

G/F Cap Building, Brgy. Corner, Osmeña Blvd.

Arlington Pond St. Extension, Cebu City, 6000 Cebu

Leave a Reply